Your Supplier’s GST Default Just Became Your Problem

And the Gujarat High Court has now made it very clear that there is no easy way out

Most of us, when we sign a purchase order, don’t spend much time wondering whether our supplier is going to pay their GST on time. We assume they will. We’ve checked their GSTIN, the invoice looks fine, the goods arrived, we paid them in full including the tax component. From our side of the table, the job is done.

Except, as a recent Gujarat High Court ruling has now reminded us, the job is not done. Not even close.

Recently, the Gujarat High Court in the case of Maruti Enterprise v. Union of India, the Court ruled on something that has been quietly bothering businesses across the country for years: the question of whether you should lose your Input Tax Credit when your supplier; through no fault of yours; fails to pay GST to the government. The answer, in short, is yes. You can. And the law that says so is here to stay.

This is, to put it mildly, a hard pill to swallow. So let’s talk about what this actually means, why the Court ruled the way it did, and what you should be doing differently from next month onwards.

*

First, a quick refresher on ITC

If you are running a business, you already know this, but it’s worth restating because the whole problem hinges on it.

When you buy something for your business, you pay GST to the supplier on top of the price. That GST you paid becomes a credit; Input Tax Credit, or ITC; which you can use to reduce the GST you owe on your own sales. The idea is simple: tax should only apply to the value you add, not the full sale price each time. It’s what stops tax from cascading down the supply chain.

For a lot of businesses, ITC isn’t small change. It can run into lakhs every month. When it disappears, working capital takes a real hit.

*

So what exactly happened in this case?

A whole bunch of businesses ; over a hundred petitions, in fact; had gone to the Gujarat High Court arguing that Section 16(2)(c) of the GST law is unfair. That’s the section which says you can claim ITC only if your supplier has actually deposited the tax with the government.

Their argument, which I think most of us would agree with on a gut level, went something like this: how on earth are we supposed to know what our supplier is doing inside the GST portal? We can’t see their GSTR-3B. We can’t make them file returns. We’ve done everything the law asks of us ; invoice in hand, goods received, payment made through banking channels. If they then choose to pocket the tax and disappear, why should we be the ones punished?

The petitioners pointed to the Delhi High Court’s ruling in On Quest Merchandising from a few years ago, which had taken exactly this view under the old VAT regime ; that you can’t penalise a bona fide buyer for the supplier’s default.

The Gujarat High Court was unmoved.

ITC, the Court said, is not a right. It’s a benefit the government grants you, on conditions. One of those conditions is that the tax actually reaches the treasury. If it doesn’t, the benefit doesn’t flow.

The Court was thorough. It went through the entire GST architecture ; how the IGST mechanism works, how money flows between origin and destination states, why the VAT-era logic from Delhi doesn’t fit here. It distinguished the old precedents and held that the GST framework, taken as a whole (Sections 16, 41, 53, 155, Rule 37A ; the lot), has its own internal balance. The system protects revenue. The buyer has remedies. The law stands.

To its credit, the Court did acknowledge that this is hard on honest buyers. It called on the government to build better tools, better tracking, real-time verification ; the sort of thing that should arguably have existed from day one. But until that happens, the legal position is what it is.

*

But I already paid the GST. How is this fair?

This is the question I’ve been asked a dozen times this past week, and I won’t pretend there’s a satisfying answer.

The Court’s reasoning, stripped down to its essence, is GST is a destination-based tax that depends on money actually moving through the system. When tax doesn’t reach the government, the chain breaks. If buyers were allowed to claim credit anyway, the originating state would end up transferring money it never received to the destination state ; and the whole settlement mechanism between states would collapse. The system, in the Court’s view, only works if there’s strict insistence on actual payment.

It’s a structural argument. It doesn’t make it feel any fairer when you’re the one losing the credit, but it explains why the Court wouldn’t budge.

There is one piece of relief built into the law, and it’s worth knowing about. Under Rule 37A, if your defaulting supplier eventually files and pays their tax ; even months later ; you can re-claim the ITC you reversed. So the door isn’t permanently shut. But you’re entirely dependent on the supplier eventually doing the right thing, which is a precarious place to be.

*

Who’s actually at risk?

Not every supplier is going to default, obviously. The risk is concentrated in a few patterns, and it helps to know what to look for.

The non-filer ; the supplier who keeps invoicing you but quietly stops filing returns. Sometimes this is genuine financial trouble; sometimes it’s deliberate. Either way, your ITC is at risk.

The collector who never deposits ; they take your tax payment but don’t pass it on to the government. This is the textbook scenario the Maruti Enterprise case dealt with, and it’s where you have the most exposure.

The cancelled-registration case ; the supplier’s GST registration was already cancelled when they invoiced you, and you didn’t check. The ITC is invalid from the start, before you even get to questions of who paid what.

The compliant supplier ; files everything on time, pays GST, shows up in your GSTR-2B exactly as expected. This is what you want, and the only way to know is to actually look.

*

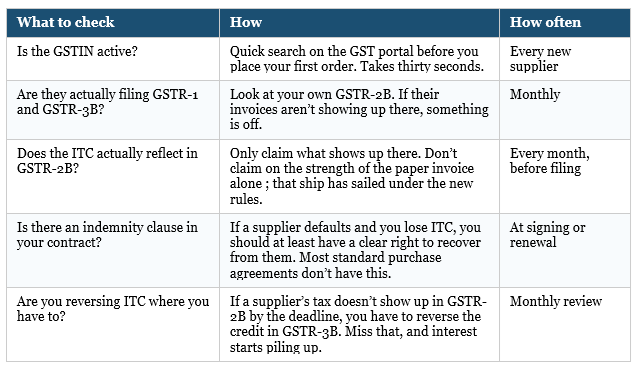

What you should actually be doing now

The Court was quite specific on this: buyers are expected to exercise due diligence. That phrase ; "due diligence" ; gets thrown around a lot, but here’s what it should look like in practice for your business:

None of this is glamorous work, and most of it falls to the same finance team that’s already stretched thin. But after this judgment, it’s no longer optional. Treat it as part of your monthly close, not a once-a-year audit thing.

The contract clause you probably don’t have

Here’s something the Court itself flagged as a practical solution, and it’s the one part of this ruling that feels genuinely useful: put a GST indemnity clause into your purchase contracts.

Most standard agreements don’t have one. They have warranties about delivery, about quality, about timelines ; but very few specifically address GST compliance. They should.

The clause doesn’t need to be complicated. The basic idea is: the supplier warrants that they will deposit the GST they collect, and if they don’t and you lose ITC as a result, they will reimburse you for the loss ; including any interest or penalty you end up paying.

This won’t prevent the ITC denial itself; the department will still come after you first, because that’s how the law works. But it gives you a clean legal basis to recover from the supplier afterwards. Without such a clause, you’re left arguing general commercial principles, which is a much harder fight.

Talk to your lawyer or adviser about what wording works for your contracts. It’s a small change with potentially significant downstream protection.

*

If you already have a demand sitting on your desk

Some of you reading this will already have received notices from the GST department denying ITC on these exact grounds. The first thing to know is that this judgment doesn’t automatically make those demands valid ; each case has its own facts, and there are usually procedural and factual angles worth exploring. Was the show-cause notice properly issued? Has the supplier since paid, allowing re-availment? Is there a contractual claim you can pursue in parallel?

What this judgment does close off is the constitutional argument ; you can no longer argue that Section 16(2)(c) is itself invalid. The provision stays. But that’s only one of several possible defences.

*

The short version

Your supplier’s tax compliance is now squarely part of your own risk management. The High Court has made it clear that this isn’t going to change ; not through the courts, anyway. Whether the government eventually builds better tools to protect honest buyers remains to be seen, and the Court has nudged them in that direction. But you can’t plan a business around that hope.

Check your suppliers. Watch your GSTR-2B every month. Update your contracts. And when something looks off, act quickly ; not at the end of the year.

It’s not the fairest outcome, but it’s the one we’re working with.

*

A small note

This is a general read on the judgment, not legal advice. The case is Maruti Enterprise v. Union of India [2026] 186 taxmann.com 90 (Gujarat), decided 1 May 2026. Every situation has its own facts; please speak to your adviser before acting on anything specific.