A New GST Rule for Intermediary Services — What It Means for You

What is an Intermediary Service?

Think of an intermediary as a middleman, someone who connects a buyer and a seller but does not directly provide the main product or service. Examples include:

• A broker who arranges an export deal between an Indian manufacturer and a foreign buyer

• An agent based in India who helps an overseas company find customers or vendors here

• A facilitator who coordinates transactions between two parties for a fee or commission

What Changed? The Big Picture

Until 30 March 2026, there was a specific rule in the GST law (Section 13(8)(b) of the IGST Act) basis which when an intermediary service is provided to someone outside India, GST would still apply because the tax was calculated based on where the service provider is located i.e., India.

This was a long-standing problem. Indian intermediaries working with foreign clients were being taxed even though they were, in effect, exporting their services. It made Indian agents less competitive globally and led to a lot of disputes with tax authorities.

The Finance Act, 2026 removes this rule entirely, effective 30 March 2026.

Now, the tax is calculated based on where the client (the recipient) is located, not the service provider. This one change has two important effects:

• If your client is outside India, your service now qualifies as an export. Such exports are not subject to GST.

• If your client is in India, the GST liability may shift to the client (under the reverse charge), depending on the situation.

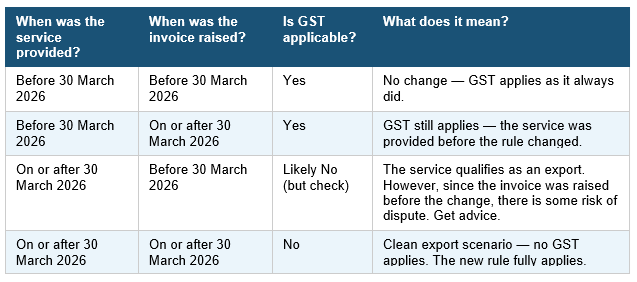

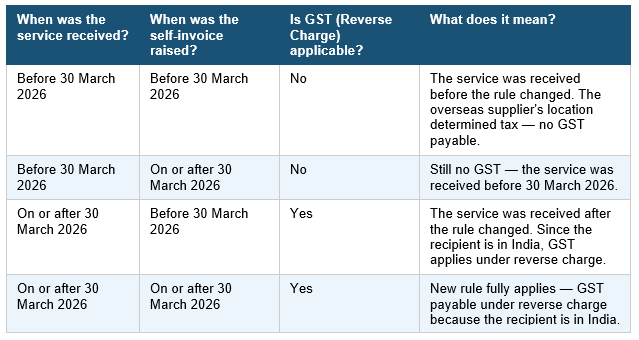

Why Does the Date (30 March 2026) Matter So Much?

Because the law changed on a specific date, transactions that happened around that date — where the service was delivered on one side and the invoice was raised on the other side — can fall into grey areas. The tables below help clarify what applies in each case.

Scenario Guide A: You Are an Indian Intermediary Providing Services to a Foreign Client

Scenario Guide B: You Are an Indian Business Receiving Intermediary Services from an Overseas Provider

What About Old Disputes and Past Tax Demands?

Many Indian intermediaries have been in disputes with the tax department for years over precisely this issue, being asked to pay GST even when their clients were overseas. Since the law that justified those demands has now been removed, there is a strong argument that those disputes should be settled in the taxpayers favour.

Important: The tax department may not give up easily on older demands. They may argue that the change should only apply going forward and not affect past assessments. If you have an ongoing dispute, do not assume it is automatically resolved, speak with your tax adviser before taking any action.

What Should You Do Now?

Here is a simple checklist to get started:

• Review your intermediary service contracts to see whether the change affects your GST position, either creating refund opportunities or new obligations.

• Check your cash flow, if you have been paying GST on services that now qualify as exports, you may be eligible for a refund.

• If you have ongoing disputes with the GST department, consult your adviser before treating them as resolved.

• Update your invoicing and accounting systems to apply the new rule from 30 March 2026 onwards.