Income Tax Act 2025 : What Changes, What Stays, and what you need to know.

India has had the same income tax statute, in one form or another, since 1961. In those sixty-five years, the Act was amended nearly 4,000 times. Provisos were added to provisos, explanations were inserted to clarify explanations that had themselves been inserted to clarify something else, and the whole structure grew to over five lakh words across 819 sections and 47 chapters. Anyone who has tried to read Section 10 of the Income-tax Act, 1961 in one sitting knows exactly what that felt like.

The Income Tax Act, 2025 is the government’s answer to that accumulated complexity. It received Presidential Assent on 21st August 2025 and comes into force on 1st April 2026. The Finance Minister announced the review in her Budget Speech in July 2024, with a straightforward stated objective: make the Act concise, lucid, easy to read, and capable of reducing disputes.

Whether it fully achieves that will only be answered through years of administration and litigation. What is clear, however, is that the statute practitioners and taxpayers will work with from April 2026 looks and reads very differently from the one that preceded it.

The Scale of What Was Done

It is said that over 150 officers worked approximately 60,000 man-hours across 26 sub-committees, each headed by a Chief Commissioner of Income Tax. The result is 536 sections against the old Act’s 819, organised across 23 chapters instead of 47, in 2.60 lakh words where there were previously 5.12 lakh. The 1,200 provisos and 900 explanations that had become the primary instrument of legal qualification in the 1961 Act are largely gone, replaced by sub-sections, clauses, 57 tables, and formulae.

“The result is 536 sections against the old Act’s 819, organised across 23 chapters instead of 47, in 2.60 lakh words where there were previously 5.12 lakh”

The language has been simplified in a meaningful way. The word “notwithstanding” has been replaced by “irrespective of” throughout. Provisos have been converted into standalone sub-sections. Tabular presentation has been used wherever the same provision applied differently to different categories of persons. A provision that previously required you to read the main section, locate the relevant proviso three paragraphs later, and then find the exception in an explanation to that proviso, now tends to sit together in a single structured block.

The parliamentary process was also substantive. The Parliamentary Select Committee held sittings in Delhi, Mumbai, and Bengaluru, received a 4,500-page report of suggestions, and the Finance Ministry responded to each of them. Many suggestions were accepted. Many were declined on the ground that they amounted to policy change rather than simplification. The Finance Ministry confirmed the governing principle clearly: existing judicial interpretation developed under the 1961 Act applies equally to the corresponding provisions of the 2025 Act.

One important note upfront. The Act as originally introduced was withdrawn after the Select Committee process, and a revised Income Tax Bill 2025 was introduced on 11th August 2025, the one that received Presidential Assent ten days later. The Finance Bill 2026 has already proposed 86 further amendments to the 2025 Act. Readers of the act should treat the current text as a live document for at least the first few months.

How the Transition Works

This is where the practical complexity is highest, and it is worth being precise about it.

The core transition rule is in Section 536 of the 2025 Act: all proceedings relating to any tax year beginning before 1st April 2026, assessments, reassessments, rectifications, penalties, appeals, revisions, continue to be governed by the 1961 Act, as if the 2025 Act had not been enacted. Penalty proceedings initiated after 1st April 2026 for earlier years still run under the old Act. Pending appeals filed against orders passed under the 1961 Act remain under the 1961 Act. The general savings provisions of Section 6 of the General Clauses Act, 1897 apply as well, preserving rights, liabilities, and obligations that arose under the old Act.

Where it gets more complex is in the situations that straddle both regimes.

On TDS, the governing principle is that the date of deduction determines which Act applies. If payment or credit to the payee occurred on or before 31st March 2026, old challans and old section references apply. For transactions on or after 1st April 2026, Section 393 of the 2025 Act governs, and deductors quoting old section numbers such as 194C, 194J, or 194H for post-March transactions will face system validation errors on the portal. The systems have been updated and they will not accept old references for new-period transactions.

On lower TDS certificates, a certificate issued under Section 197 of the 1961 Act remains valid for payments made on or after 1st April 2026, provided it was issued for the projected receivable for Tax Year 2026-27.

On losses and depreciation, the carry-forward framework is preserved. Losses under business income, house property, speculation, and specified business activity up to Assessment Year 2026-27 are to be set off and carried forward in the manner prescribed under the 1961 Act. Unabsorbed depreciation and capital expenditure on scientific research are to be added to the allowance for Tax Year 2026-27. The continuity of deductions under Sections 35ABB, 35D, 35DD, 35DDA, and 35E is explicitly preserved.

Any election, declaration, or option made and in force under the 1961 Act is deemed to have been made under the corresponding provision of the 2025 Act. All circulars, orders, instructions, and notifications issued under Section 119 of the 1961 Act continue to have effect to the extent not inconsistent with the 2025 Act.

One point on limitation that is easy to miss: where a limitation period had already expired under the 1961 Act, no extension arises simply because the 2025 Act prescribes a longer period. Time already lost is lost.

The Income Tax Department launched a new website on 20th March 2026 with a comprehensive set of transition FAQs. The e-filing portal will facilitate compliance under both Acts concurrently. Practitioners should make the transition FAQ portal their first reference for procedural questions in the coming months.

Key Changes in the Statute

Tax Year

The 2025 Act introduces the “tax year” in place of the previous year and assessment year. The tax year corresponds to the financial year in which income is earned. What was previously Assessment Year 2027-28 is now Tax Year 2026-27. The underlying mechanics are unchanged. For practitioners accustomed to thinking in assessment year terms, the adjustment is primarily one of habit.

Residential Status

Section 6 has been rewritten in cleaner language, but the substance is unchanged. The 182-day test and the 60-plus-365-day test remain. The deemed residency rule for Indian citizens not liable to tax in any other country, applicable where total income exceeds Rs. 15 lakh from non-foreign sources, is retained in the same form. The Not Ordinarily Resident category survives, though its practical utility remains limited outside the context of returning NRIs.

Exemptions in Schedules

Section 10 of the 1961 Act, which ran to over 100 pages and covered everything from agricultural income to provident fund receipts to IFSC exemptions, has been reorganised into eight schedules numbered II through VIII. The structure now groups exemptions by category of person and type of income rather than presenting them as one undifferentiated list.

Schedule II covers general exemptions available to all taxpayers: agricultural income, life insurance proceeds, provident fund, NPS withdrawals. Schedule III covers exemptions for specific eligible persons such as HUF distributions, partnership profit shares, and minor income. Schedules IV through VIII address non-residents, AIFs and business trusts, IFSC entities, persons entirely exempt from tax, and political parties respectively.

The substance of the exemptions is largely preserved. The reorganisation makes it considerably easier to identify what applies to a given taxpayer.

Presumptive Taxation

Section 58 consolidates the three presumptive taxation regimes, old Sections 44AD, 44ADA, and 44AE, into a single section with a table. The rates and limits are unchanged.

One substantive change worth noting: the requirement to maintain books of account and get them audited when a taxpayer claims income below the presumptive rate has been extended to all three categories of presumptive taxpayers. Under the 1961 Act, this obligation was largely limited to professionals under Section 44ADA. The compliance footprint for taxpayers who deviate from the presumptive rate in any year has widened.

Unexplained Incomes and Virtual Digital Assets

Section 104 of the 2025 Act, corresponding to Sections 69A and 69B of the 1961 Act, now explicitly includes virtual digital assets within the scope of unexplained assets. A new Section 107 provides for the chargeability of such incomes. This is not a surprise. The Department has been clear for some time that it views VDAs as identifiable, seizable assets, and the explicit statutory inclusion removes any remaining ambiguity.

Deductions

The Section 80C family of deductions, old Sections 80C, 80CCA, and 80CCB, is now consolidated in Section 123 read with Schedule XV, which sets out in tabular form the eligible investments, the conditions for withdrawal, and the taxation of receipts where deductions were previously claimed. NPS deductions have their own dedicated provision in Section 124. Section 80D maps to Section 126, Section 80G to Section 133, Section 80JJAA to Section 146, and Section 80M to Section 148. The substance is unchanged. The location has shifted.

MAT and AMT

Sections 115JB, 115JAA, and 115JC through 115JF, the MAT and AMT provisions, have been merged into a single Section 206. The rates across different taxpayer categories are presented in a single consolidated table.

The substantive change here is significant: from Tax Year 2026-27, no further accrual of MAT credit will take place. MAT becomes a final tax liability. For companies transitioning to the new regime, utilisation of past MAT credit is limited to 25% of tax payable in any given year. For foreign companies, MAT credit is available only to the extent of MAT liability, with no further accrual.

Companies sitting on large MAT credit balances need to model the impact of this change before the Tax Year 2026-27 return cycle. The planning window is closing.

Reassessment

Section 280, corresponding to Section 148, has been expanded in one significant respect: the scope of “information” that can trigger a notice of reassessment now includes any direction given by the GAAR Panel and any finding or direction contained in an order passed by any authority, tribunal, or court under the Act or under any other law. Where these two new categories apply, the pre-notice inquiry procedure under Section 281, the old Section 148A process, does not apply. The time limits for issuing reassessment notices remain unchanged at four or six years from the end of the relevant tax year.

Search and Survey

The search and survey provisions have been updated for a digital operating environment. Section 247, corresponding to old Section 132, now explicitly covers assets held in virtual form, virtual digital assets, data stored in electronic media, and information in computer systems including virtual digital space. Authorised officers can now override access codes to computer systems, direct persons to provide technical assistance including access credentials, and pass prohibitory orders over bank lockers and accounts. Survey provisions under Section 253 carry similar digital extensions and now permit statements to be recorded on oath.

TDS

All TDS provisions are now under a single Section 393, with sub-section-wise tables for different payment categories.

The phrase “likely to be paid or credited during the year” has been removed. TDS now applies only when actual payments exceed the threshold, without regard to projected future payments. Cash withdrawal thresholds have been simplified: the earlier two-tier structure, with a lower limit of Rs. 20 lakh for non-filers, has been replaced by a common limit of Rs. 3 crore for all non-cooperative society persons. Applications for lower TDS under the new Section 395 can now be made for all types of payments, unlike old Section 197. The correction statement filing window has been reduced from six years to two years from the end of the tax year. TCS is now collectible at the time of debit or receipt across all transaction types.

Charitable and Religious Trusts: The Most Consequential Change

The overhaul of the charitable trust taxation framework is, in terms of practical complexity and client impact, the most significant change in the 2025 Act. Every registered trust, institution, and non-profit organisation needs to understand this before filing the Tax Year 2026-27 return.

The two parallel regimes under the 1961 Act, the general exemption route under Section 11 for trusts registered under Section 12A/12AA/12AB, and the Section 10(23C) route for approved funds, educational institutions, and hospitals, have been merged into a single framework under Chapter XVII-B: Special Provisions for Registered Non-Profit Organisations, spanning Sections 332 to 355.

The fundamental conceptual shift is this: the 2025 Act moves from a framework of exemption to a framework of computation. A registered NPO is no longer exempt from tax in the conventional sense. Instead, its income is computed in a specific manner, with the result that most income ends up being tax-nil if the compliance conditions are met, and taxable if they are not.

The income of a registered NPO is classified into three categories.

The first is regular income, which includes income from charitable or religious activity for which the NPO is registered, income from property or deposits held for those purposes, voluntary contributions received, and gains from permissible commercial activity.

The second is specified income, a list of 11 specific situations covering anonymous donations above the prescribed threshold, income applied for the benefit of related persons, investments in non-permitted modes, and violations of corpus donation conditions. Specified income is taxed at 30%.

The third is residual income, everything that does not fall into the first two categories, taxed at the applicable rates.

The 85% application rule remains: where 85% or more of regular income is applied for charitable or religious purposes or formally accumulated under Section 342, the taxable regular income is nil. Where the application falls short of 85%, only the shortfall is taxable.

On commercial activity, the regulation is now sharper. Non-GPU organisations, those with specific charitable purposes such as education, medical relief, or yoga, may carry out commercial activity only if it is incidental to their objects and only if separate books are maintained. GPU organisations, those advancing any other object of general public utility, may carry out commercial activity only if it arises in the actual course of advancing that GPU object, aggregate receipts from such activity do not exceed 20% of total receipts for the year, and separate books are maintained.

A violation of the 20% limit for GPU organisations results in taxation of the net income from that activity. It does not result in cancellation of registration, as clarified by the Finance Act 2026 amendment. Violations by non-GPU organisations of the incidental business condition, however, can result in cancellation.

A new common audit report, Form 112, has been introduced for all registered NPOs, with separate columns for large and small organisations.

Income Tax Rules, 2026

The Income Tax Rules, 2026 were notified on 20th March 2026 and take effect from 1st April 2026. The structural reduction mirrors the Act: 333 rules against 511, and 190 forms against 399.

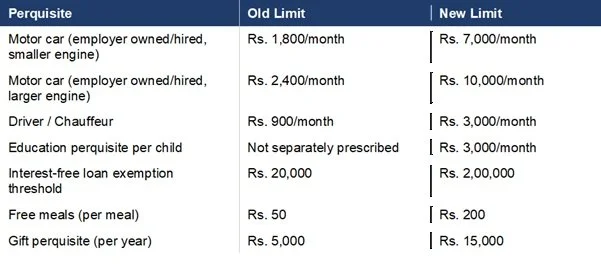

Several long-overdue perquisite limits have also been revised. These affect payroll computations across virtually every employer and need to be built into systems before April 2026.

Forms 15G and 15H have been combined into a single Form 121. Chartered Accountants can now register as valuers for shares and securities under the new rules.

What Needs Attention Now

The transition to the Income Tax Act, 2025 is not a single event. It will run through the entirety of Tax Year 2026-27 and beyond. Several things require attention immediately.

For all employers and deductors, TDS systems must be updated before 1st April 2026 to reference the new section numbers under Section 393. Using old section references for post-March transactions will generate system errors. Payroll systems must incorporate the revised perquisite values from the same date.

For companies with accumulated MAT credit, the modelling needs to happen now, before the Tax Year 2026-27 return is filed. The 25% annual cap on utilisation means that large credit balances may take several years to exhaust, and the planning around regime choice and utilisation sequencing has real financial consequences.

For every charitable trust, educational institution, hospital, and religious organisation registered under Section 12A, 12AA, 12AB, or Section 10(23C) of the 1961 Act, the transition to the Chapter XVII-B framework requires a structured review of the existing setup: the objects clause, the corpus investment structure, related-party benefit arrangements, commercial activity exposures, and compliance with the application and accumulation rules. The first audit report and return under the new framework will be filed in September and November 2026 respectively. The preparation window is now.

For practitioners handling assessments and litigation, every proceeding needs to be correctly characterised by which Act governs it. Orders passed under the 1961 Act, appeals flowing from them, and penalty proceedings for pre-April 2026 years all remain under the 1961 Act. The systems and portals will enforce this distinction, but the judgment about which framework applies in any given situation still rests with the practitioner.

Closing Thoughts

The Income Tax Act, 2025 is a serious piece of legislative work. It does not solve every problem with the 1961 Act. Provisions that were substantively ambiguous in their old form have largely been carried across in their new form, and the areas of genuine policy complexity remain areas of complexity. But for a statute that had become genuinely difficult to navigate, the restructuring is a real improvement.

What the Act does not do is make the tax system simpler in the economic or substantive sense. The same incomes are taxed, at broadly the same rates, with broadly the same deductions and exemptions. The simplification is in presentation and structure, not in the quantum of obligation. That was always the stated objective, and on that measure, it has largely been achieved.

The next few months will define how smooth the actual transition turns out to be. CNK RK & Co. is actively working with clients across all aspects of this transition: TDS system updates, MAT credit planning, charitable trust restructuring, and the full range of cross-border and domestic tax advisory that the new Act touches. We will continue to publish guidance as the position evolves.